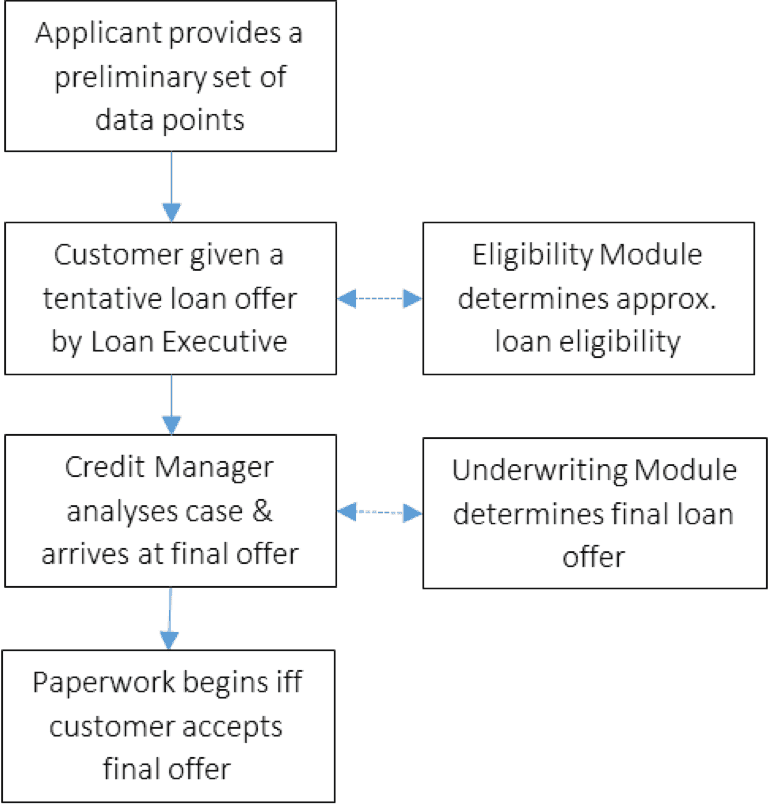

Data points collected from an applicant at the outset are,

The Eligibility Module gives maximum loan amount (tentative) that can be given to this applicant and also the associated tenor. Also, the EMI and the break-down of the EMI into principal and interest components are made available by this module. The team tells the applicant the time taken for the entire loan process (eventually leading to the disbursement).

The Loan Executive communicates the following to the applicant verbally,

Note: The Eligibility Module has a propriety Debt Burden Ratio (DBR) range set on the salary of the applicant. This, in conjunction with other variables, gives the maximum possible (additional) debt that an applicant can service

A loan offer is emailed to the applicant and the loan application of the applicant (henceforth called the case) reaches the Sales Manager (SM).

The SM checks for the following documents in the order of priority,

The case now reaches the Credit Manager (CM) who now pulls the credit report computed/created by CRIF Highmark Bureau.

If there is any write-off/settlement in the past one year, the case is dropped/rejected.

This is done through a software called Perfios and an internal tool built to analyse and tabulate the data derived from Perfios. The following are checks are performed,

i. Payment history: CM can the regularly of past repayments etc

ii. Payslips matching: the payslip amount is compared with the bank cash inflow into the salary bank account

iii. Loans, EMIs, credit card(s) & their payment, and informal loans etc: recently taken loans, cheque bounces, cash outflow to specific accounts etc are used to determine current monthly liability (formal & informal (and to get a glimpse of repayment behaviour on old loans

iv. Bank balances: to see if the customer will be able to pay the EMI amount.

a. Minimum average bank balance per month should be >= INR 1,000

b. Average bank balance on specific dates of the month

The CM talks to the customer and seeks answers to the questions that arise during the case analysis. The CM also tries to gauge the intent of the customer to repay the loan.

The final loan eligibility is determined now. This might be less or greater than the tentative offer given to the applicant earlier.

The next steps include house verification, putting the loan up for receiving lender interest on the Cashkumar platform, agreement creation and shipping of hard copies, receiving the house verification report, final check of all documentation and, finally, loan disbursement to the applicant (now called the borrower).